Buying a Condo? Focus on the Financials

Condominiums, or condos, appeal to home buyers of all ages and life stages, but they are especially attractive to younger families and retirees who want to reap the benefits of homeownership while spending less time and money on upkeep.

Residential condos are typically individually owned apartments in multi-family buildings, but a condo is a form of property ownership, not a type of housing. Condos may also be attached or detached single-family units within a community. Each owner generally owns and maintains the interior of the unit and has a shared interest in exterior and common areas which are maintained by the community, such as the roof, lobby, and landscaping, and any amenities such as a fitness center, clubhouse, and pool.

Prices vary, depending on market and other factors, but condos are generally priced lower than single-family houses. In 2024, the median price of a condo was about 12% less than a single-family home.1 But that doesn’t necessarily mean you’re getting more bang for your buck. Condo ownership comes with some special costs and financial implications.

Factor in condo fees

In addition to making mortgage, condo insurance, and real estate tax payments, condo owners typically pay ongoing, mandatory fees (called assessments) to a condo association (COA) or homeowners association (HOA) to cover the costs of running and maintaining the community. Part of the fees collected often go into a reserve fund, which is money set aside to cover unexpected expenses.

On occasion, condo owners may be required to make a one-time payment in addition to regular monthly fees. This special assessment may be necessary when there is not enough money in the reserve fund to cover a large or unexpected expense.

When you’re buying a condo, it’s important to understand that fees are likely to go up each year, as maintenance and upgrade expenses, utility costs, and insurance premiums for the community increase. Fees vary widely, but condo fees that seem especially low in comparison to similar communities could be a red flag. Perhaps residents are unwilling to pay more to strengthen reserves or maintenance is being deferred, which is a serious issue that can lead to critical, expensive repairs and diminish the property’s resale value. On the other hand, condo fees that seem especially high could also be a problem — will they become unaffordable if they continue to rise? High condo fees could also deter future buyers.

Look at appreciation potential

Like single-family homes, condos may appreciate in value over time. In 2024, condos appreciated 2.9% on average, while single-family homes appreciated 5%.2 Of course, real estate appreciation fluctuates, depending on market conditions, and depreciation is also possible. Before you make an offer, consider current value, market trends, location, size, age, condition, recent improvements, and whether any assessments might affect the future value.

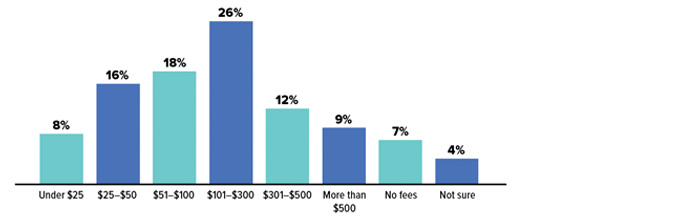

Monthly fees reported by COA and HOA members

Source: Foundation for Community Association Research, 2024 Homeowner Satisfaction Survey. Fees were reported as part of a nationwide survey; they may not reflect average fees in your area. COA fees are typically higher than HOA fees because they must cover extra services and additional maintenance costs.

Other considerations

Work with a knowledgeable real estate professional. Someone who knows the condo market well can help you navigate the buying process. This includes doing a comparable sales analysis and pointing out positive or negative factors that could affect future costs or appreciation potential.

Review condo documents. These will spell out community rules and regulations (called covenants, conditions, and restrictions) and bylaws. Also review financial statements to help ensure that the community is adequately funded, and ask questions.

Explore financing options. Getting a mortgage for a condo is generally similar to getting one for a single-family home, but there are some different rules and qualifications. For example, the condo community must meet lender guidelines, so the lender may ask to review the community’s proof of insurance, financial statements, and condo documents. Interest rates and costs may vary, and not every lender will finance condominiums, so you’ll need to shop around.

Understand rental rules if you plan to rent out your condo. Some communities ban rentals, while others may have limits on the length of a lease or the percentage of owners who are able to rent their units.